A Reflection on Money, Mortality, and Meaning

Savings Vs living in the present! As finance person I look back and wonder if I should be delivering this article, afterall I am a strong believer in saving and investment. But I want to share about the other realities!!. We spend our lives being told to save for tomorrow, “max out those retirement accounts, build an emergency fund, prepare for a future that promises security and comfort”. Every financial planner, self-help book, and motivational speaker emphasizes the importance of setting aside money for a rainy day. Yet, an uncomfortable question rarely gets asked: What if tomorrow never comes? What if all those shillings, pesos, yens, dollars, diligently stashed away in the name of future security, never actually serve you because you never get to live the life you’re saving for?

The Reality of Life’s Uncertainty

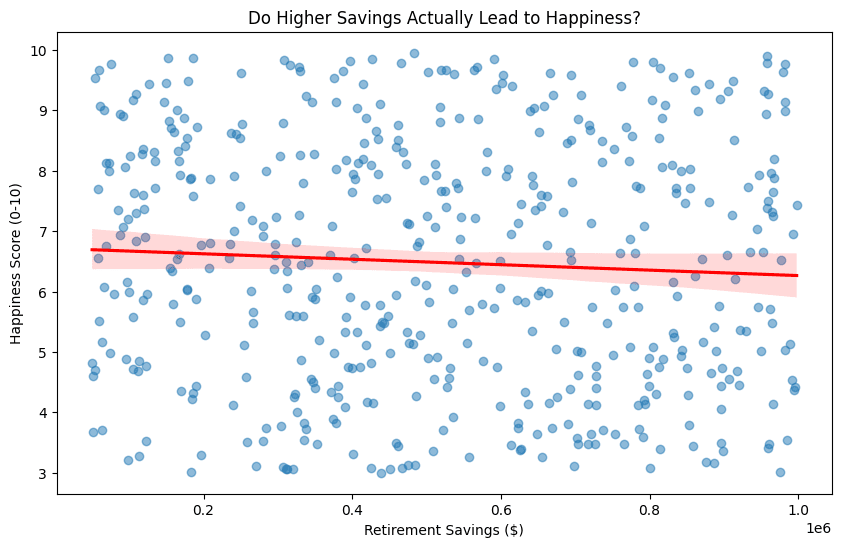

Consider this, one in five Americans dies before reaching retirement age. It’s a sobering reminder that our time on earth is uncertain. Even more astonishing is that many retirees leave behind inheritances they never intended to pass on, not out of generosity, but simply because they couldn’t spend it all in time. We spend hours dissecting investment strategies, diversifying portfolios, and chasing the ever higher rates of return, yet seldom pause to ask the harder question, What if all this saving is for a life I won’t get to live?

The Stories of David and Maria

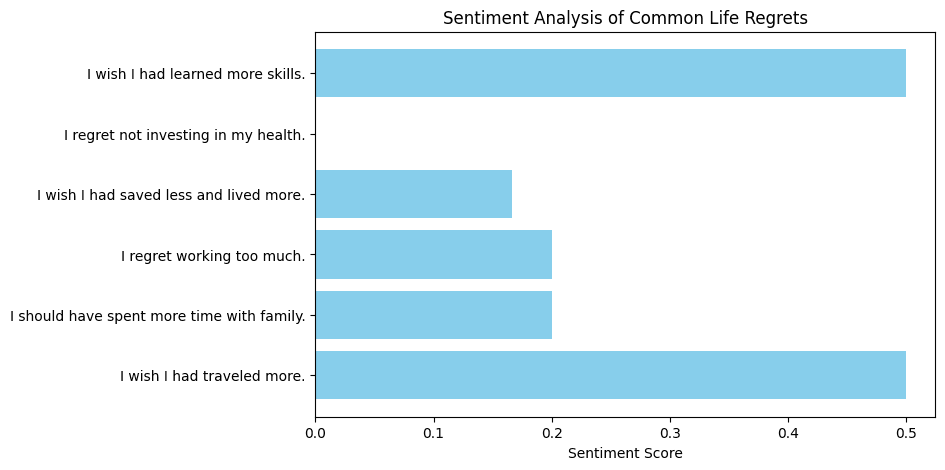

David, a dedicated corporate lawyer who prided himself on saving 40% of his income for decades. In the eyes if the world, which we love so much, by all conventional measures, he was a success. But at 58, David received a devastating diagnosis, knock knock – pancreatic cancer. In his final days, his regret wasn’t about missing investment opportunities or not accumulating enough wealth. Instead, his heartfelt admission was, “I wish I had taken the damn trip to Kyoto.” David’s hard-earned wealth had become a barrier to the experiences he truly longed for.

Contrast this with Maria, a schoolteacher who many considered fiscally irresponsible and financially illiterate, because she “wasted” money on family reunions and get togethers. Maria embraced life, valuing moments with her loved ones over the accumulation of wealth. When she died suddenly at 60, her children recalled those cherished trips back home as the true legacy of her life, a collection of memories that money simply could not buy.

The Irony of Financial Planning

This irony is profound, while we insulate our cars and homes with insurance policies that guard against every conceivable risk, we rarely take measures to safeguard our dreams against the greatest risk of all, never actually living them. Our financial habits often reflect a deep seated fear of scarcity, a constant worry that we might one day run out of money. Yet, in doing so, we may be sacrificing the richness of life in pursuit of a phantom future.

The Deferred Life Plan Vs. The YOLO Disaster

Most people approach money in one of two ways, both of which often lead to regret.

- The Deferred Life Plan

It is a mindset that equates happiness with a future reward. “I’ll travel after I retire,” or “I’ll splurge once I hit my savings goal.” This approach turns life into a perpetual waiting game. - The YOLO Disaster

An impulsive, short-sighted approach that values immediate gratification over long-term stability. “Life’s short!” becomes the rallying cry for reckless spending. While living in the moment has its merits, unbridled spending can lead to financial stress.

The Smile Test: Are You Saving Too Much?

Let us start with the Smile Test. When you look at your bank statement, does the number fill you with a sense of pride and security, or does it evoke anxiety and a feeling of confinement? May its not on the account, who keeps their money on the account these days, it could be in the unit trust or investment brokerage account. I once met a couple with a net worth of two hundred million Ugandan Shillings (or dollars, depending on your context) who were so terrified of “running out” that every night they resorted to eating nothing but canned beans and street food – rollex . Their wealth, instead of being a source of liberation, had become a prison.

Calculating Your “Enough Number“

Your Enough Number is the amount of money you truly need to feel secure. For some, this might equate to let’s assume $2,000 per month in retirement. At a safe 4% withdrawal rate, that translates to a nest egg of roughly $600,000. Is if you do not assume any investment return in retirement , this could last 25 years. Any money saved beyond this should not be hoarded as a buffer against uncertainty but allocated toward experiences that enrich your life.

The Deathbed Question

A 2022 study published in The Journal of Positive Psychology revealed that 82% of people’s deathbed regrets fall into two categories of wishes, “I wish I’d taken more risks.” and “I wish I’d let myself be happier.”

Notice something intriguing, financial regret rarely makes the list. People measure the worth of their lives not by the size of their bank accounts but by the quality of their memories and relationships. A true test to savings vs living in the present!

Strategies to Break Free from Over-Saving

- The 5% Rule

Dedicate 5% of your investment portfolio to experiences today. This ensures that you’re actively investing in happiness, not just wealth. - Health-Adjusted Spending

Recognize that certain experiences are more valuable when you’re in good health. Then adjust your spending on experiences accordingly, to suite the needs and demands. - Give While You Live

Instead of hoarding money for an inheritance, use part of your wealth to fund experiences for your family and community now.

The True Measure of Wealth

Some critics argue, “What if I live to 100?” That’s a valid concern, which is why the goal isn’t to spend everything but to strike a balance. The real risk isn’t running out of money; it’s optimizing your life for a 100 year existence while actually living only 70 years filled with “what ifs.”

Money is a tool, not a trophy. The ultimate aim of saving is not to die with the largest bank balance but to live a life with the fewest regrets. Spend on what matters most: time with loved ones, health, personal growth, and memorable experiences.

What’s Your Challenge: A Life with No Regrets

This week, do one thing your future self will thank you for. Perhaps it’s booking that long postponed trip, hiring help to carve out time for yourself, or donating to a cause close to your heart.

The ultimate measure of wealth isn’t your net worth—it’s your “no regrets” score.

Imagine your 80-year-old self looking back. Will they thank you for working tirelessly for every penny, or will they appreciate the moments of joy and risk that you embraced?

Define your “enough,” invest in your experiences, and dare to live without regrets. Because when your time comes to look back, the memories you create and the relationships you nurture will be the true markers of a life well-lived.

Savings vs living in the present! See ideas on passive income