How do I get here?

Stocks!! A recent claim that the Bourse Régionale des Valeurs Mobilières (BRVM), West Africa’s stock exchange, outperformed NSE over the past decade sparked interest. So out of selfishness and the East African spirit, I set out on a journey to establish facts. This analysis compares African stock markets, focusing on returns, volatility, responsiveness to global shocks, and the hypothetical performance of a $1,000 investment. The data covers the period from 2016 to 2024.

What is the BRVM and NSE?

To put records straight, we are not talking about the NewYork Stock Exchange but rather the Nairobi Stock Exchange!!. The BRVM is a unique regional stock exchange serving eight West African Economic and Monetary Union (WAEMU) nations, which are Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal and Togo. It operates electronically, offering regional diversification but faces risks from political and economic diversity.

Kenya’s NSE is East Africa’s most structured stock market, benefiting from economic stability and strong regulatory oversight. However, it struggles with liquidity challenges and limited company listings. Both markets reflect their regions’ economic strengths and weaknesses.

Challenges in Assessing African Stock Markets

For the analysis, I faced a number of hurdles, including data scarcity, inconsistent listings, and currency volatility. The process lasted longer than expected, but I guess I am also good at procrastinating! Despite these challenges, it seeks to answer two key questions:

- Is it profitable to invest in African stock markets?

- How would an investment of a similar amount of USD 1000 have performed across different markets?

- Lets forget the NSE Vs BRVM question, but it was overtaken by more important analyses

Disclaimers and Market Context

The study focuses on the performance of market indices rather than individual companies listed on the stock exchanges. As you may agree, these indices serve as representations of the overall market performance for their respective countries.

Stock market performance is not a direct indicator of economic growth in Africa. Most of the companies are privately owned and these drive a lot of growth across the continent. Also, not many of the continent’s inhabitants are invested in stocks, stock markets represent only a fraction of investment opportunities in the structured markets universe. Other options for investments include bonds, private equity, and commodities, not to forget private equity. Of late many Ugandans are excited about bonds and unit trusts. Other investments outside this universe can be property , agriculture, trade, services to mention

Moreover, African markets often deviate from the efficient market hypothesis. Stock prices may not immediately reflect or factor all available information in the markets. For example, scandals or government announcements may have delayed or minimal impacts on share prices, unlike in developed markets.

Scope of the Analysis

This study focuses on indices from Kenya, Egypt, Mauritius, Ghana, Botswana, Tanzania, Rwanda, Uganda, Malawi, Zambia, Tunisia, BRVM, Nigeria, and Morocco. Zimbabwe, Ethiopia, Algeria, SouthAfrica and Libya were excluded due to data in-availability.

Currency Impact on Returns

The performance of the various indices was analyzed both in local currencies and USD to enable a more comparable evaluation. For this, indice prices were converted using the prevailing exchange rates during the entire period under review. Currency fluctuations significantly influence stock market returns. For instance, Malawi’s Kwacha (MWK) exchange rate fluctuated between 720 and 727 MWK per USD between February 23 and March 29, 2017. This fluctuation was likely driven by external debt, trade imbalances, and global economic conditions (feel free to share additional insights on what happened in Malawi in the comments). This example highlights how currency depreciation can erode USD-based returns, even in markets experiencing nominal growth. Many African markets face similar challenges, where weak local currencies diminish real returns despite stock market growth in nominal terms. That said, the comparison of returns in local currency and USD showed minimal differences, as return is unitless and expressed as a percentage change.

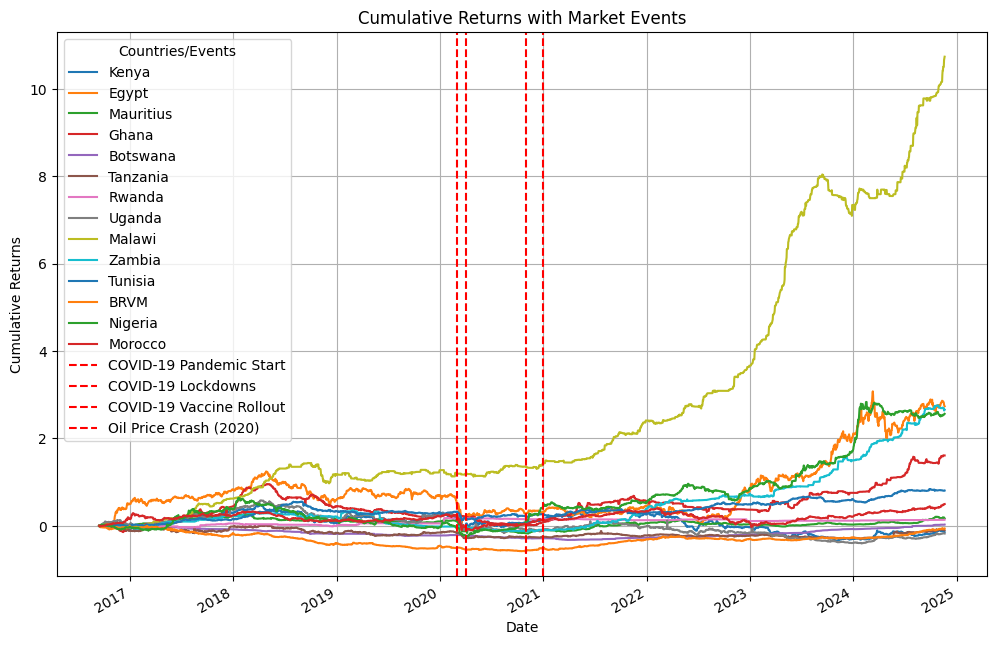

The Impact of Global Events on African Stock Markets

Graphical data suggests minimal responses to global events, but detailed analysis reveals some real impacts. Pre- and post-event means, T-statistics, and p-values highlight these effects. The events analyzed include:

- March 2020: COVID-19 Pandemic Start

- April 2020: COVID-19 Lockdowns

- November 2020: COVID-19 Vaccine Rollout

- January 2021: Oil Price Crash (2020)

The COVID-19 pandemic significantly impacted African stock markets, with varying responses across countries. In March 2020, initial reactions mirrored global trends, with sharp declines as uncertainty dominated markets. However, recovery patterns varied. Domestic sectors like banking and agriculture rebounded faster in some regions due to lower reliance on global supply chains. The BRVM showed resilience, likely due to its focus on industries less exposed to global volatility.

Event-Based Effect on Stock Market Analysis

Kenya’s returns shifted positively after the pandemic’s onset, with a mean increase from -0.0926 to 0.1016 (p = 0.0166). Mauritius experienced a marginally significant negative change (p = 0.0527). Most other countries showed no statistically significant changes during this period.

Lockdowns negatively impacted Tunisia, with a significant decline in returns (p = 0.0434), while other countries showed negligible changes. The vaccine rollout led to marginally significant shifts in Egypt (p = 0.0688) and Uganda (p = 0.0692), though responses in most markets were insignificant.

The 2020 oil price crash significantly affected Tunisia (p = 0.0383) and the BRVM (p = 0.0888). However, other countries showed no notable effects during this period.

These findings demonstrate that the pandemic and related events had mixed and uneven impacts on African stock markets. Regional differences in industrial structure, policy responses, and external vulnerabilities influenced market performance. Kenya and the BRVM displayed resilience, while others struggled to recover.

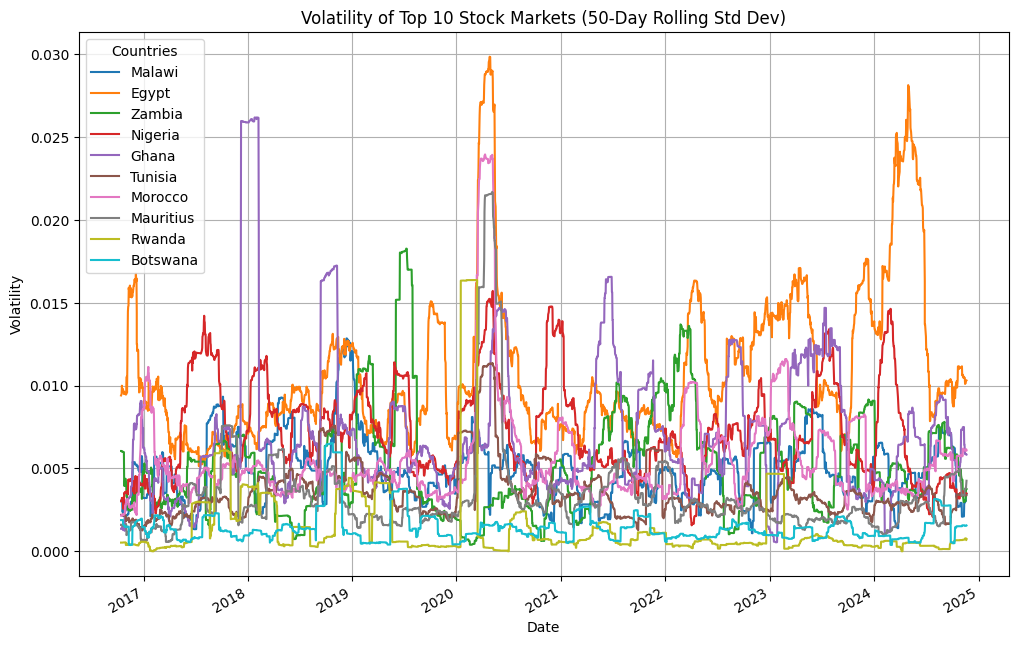

Volatility Analysis of African Stock Markets

Volatility in African stock markets shows significant variation, influenced by unique economic conditions and market structures. Based on mean values, Rwanda (0.0014) and Botswana (0.0014) exhibit the lowest volatilities, indicating extremely stable investment environments. These markets are particularly appealing to risk-averse investors seeking minimal fluctuations.

Malawi, with a mean volatility of 0.0049, shows higher fluctuations compared to Rwanda and Botswana but remains relatively stable. In contrast, markets like Egypt (0.0108) and Zambia (0.0052) demonstrate significantly higher volatility, reflecting frequent market swings. These fluctuations may result from macroeconomic challenges or political instability, offering opportunities for higher returns but with elevated risks.

Markets such as Mauritius (0.0032) and Tunisia (0.0035) display moderate volatility, balancing growth potential with manageable risks. These markets are generally attractive to investors seeking both stability and modest returns.

Between November 15-20, 2024, Botswana and Rwanda maintained consistently low volatilities, ranging between 0.0007–0.0016, reaffirming their low-risk profile. Malawi’s volatility ranged from 0.0030–0.0035, showing a stable but slightly riskier environment. Conversely, Egypt and Zambia experienced volatility levels from 0.0101–0.0103 and 0.0030–0.0038, respectively. These higher fluctuations indicate greater short-term risks but the potential for substantial returns.

The analysis highlights the diverse risk-return profiles of African stock markets. While some markets like Rwanda and Botswana offer stability, others like Egypt and Zambia present higher-risk, higher-return opportunities. Investors can tailor their strategies based on their risk tolerance and investment goals.

Correlation of Stock Markets Across African Nations

The correlation matrix between various African stock markets provides insight into how interconnected these markets are. Markets with higher positive correlations tend to move in similar directions, while those with negative correlations or near-zero correlations suggest divergent performance patterns.

For instance, Kenya and Uganda exhibit a positive correlation of 0.1049, indicating that the two markets tend to experience similar trends. This could be due to shared regional economic factors or similar industry compositions. Conversely, countries like Rwanda and Malawi show a near-zero correlation, with a value of -0.0575, suggesting that their market movements are largely independent of each other.

Countries like Egypt and Morocco have a moderate correlation – 0.1228, meaning they may share some common factors influencing their stock market trends, yet they also exhibit distinct behaviors. In contrast, markets like Nigeria and Tunisia show low to moderate correlations with other African markets, indicating that external factors or local dynamics significantly impact their stock performance independently of regional trends for where they are situated.

If you are an investor looking to diversify your portfolios across Africa, you could benefit from these correlations, as combining stocks from countries with low correlation to each other can help reduce overall portfolio risk. For instance, pairing stocks from Botswana with low correlation with other markets with those from Egypt or Kenya could create a more resilient investment strategy, balancing the volatility and market-specific risks.

The correlation analysis highlights the diverse performance patterns of African stock markets, underscoring the importance of regional integration for fostering economic growth and stability. Many African stock markets show low to moderate correlations, suggesting that they often react independently to local and global economic events. This lack of synchronicity can present both challenges and opportunities for investors, as it creates potential risks related to country-specific volatility but also opens avenues for diversification.

Regional integration

Talking about correlations, let us see how it affects regions. Since I come from EastAfrica, I know how hard it is to find Anglophones in francophone countries purely doing private business. Stock markets within the same regional or geographical groups exhibit varying levels of correlation, reflecting both similarities and disparities in their market dynamics. In East Africa, for instance, Kenya, Uganda, and Tanzania share moderate correlations, such as Kenya-Tanzania (0.096) and Kenya-Uganda (0.105), likely due to economic integration within the EAC (East African Community). However, Rwanda, also in East Africa, shows very weak correlations with its neighbors (e.g., Rwanda-Kenya at 0.006), highlighting its smaller market size and limited cross-border market linkages. Similarly, in West Africa, Nigeria has weak correlations with the BRVM (0.011), despite geographic proximity, as the BRVM operates under the CFA franc and targets francophone markets, while Nigeria’s market is anglophone and operates independently. In North Africa, Morocco and Tunisia show moderate correlation (0.077), reflecting shared economic conditions, but correlations with Egypt are lower (e.g., Morocco-Egypt at 0.123), suggesting distinct market drivers. These patterns illustrate that while proximity can enhance market integration, linguistic, economic, and institutional differences can still create significant disparities.

To mitigate these risks and enhance economic resilience, greater regional integration is essential. By strengthening ties between African nations through initiatives like cross border trade agreements, infrastructure development, and financial market collaboration, countries can harmonize their economic policies and create more interconnected markets. Though on the other hand this also has its challenges but poses more benefits. Increased regional cooperation can also help smooth out the volatility observed in isolated markets by providing access to a broader range of assets, industries, and economic conditions that collectively improve the investment climate.

Furthermore, regional integration could help in reducing the negative impacts of economic shocks in one country on others within the region. For instance, a country experiencing political instability or a sharp economic downturn could benefit from the stabilizing influence of more robust regional markets, leading to a more synchronized response to such events. Though the argument is that one bad egg, could also spoil the party for the rest of the regional group members.

In the long term, a more integrated African market could also attract foreign investors who are sometimes hesitant due to the fragmentation and varied risks across individual countries. Stronger regional financial infrastructure would allow for better liquidity, easier capital movement, and more robust diversification opportunities, thus making the entire region more attractive as a single investment destination. Ultimately, regional integration could be the key to unlocking the full potential of African stock markets and contributing to sustainable growth across the continent.

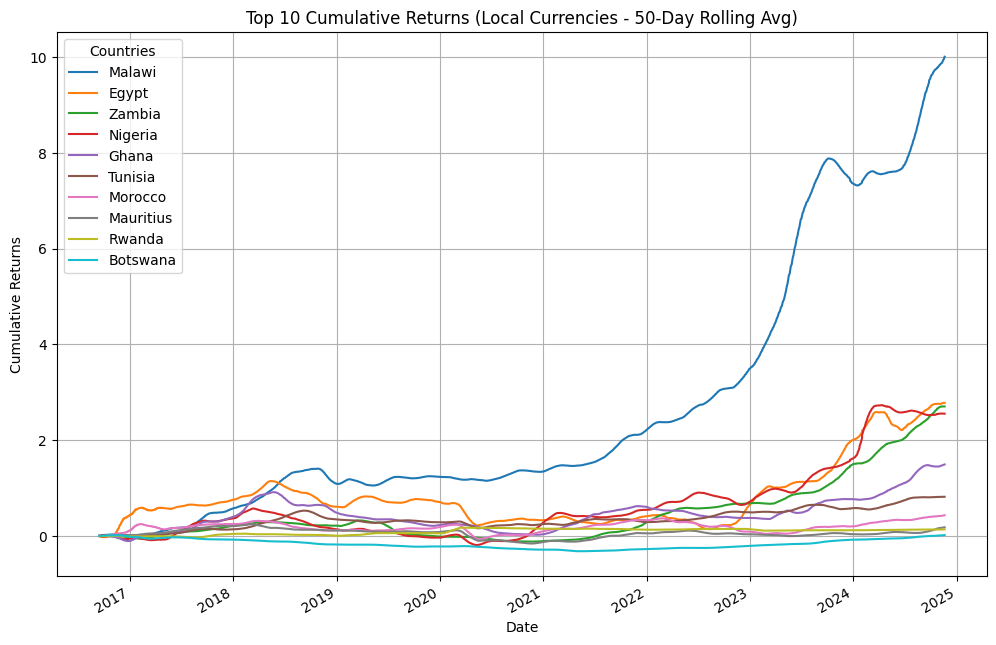

Cumulative stock returns across various African markets

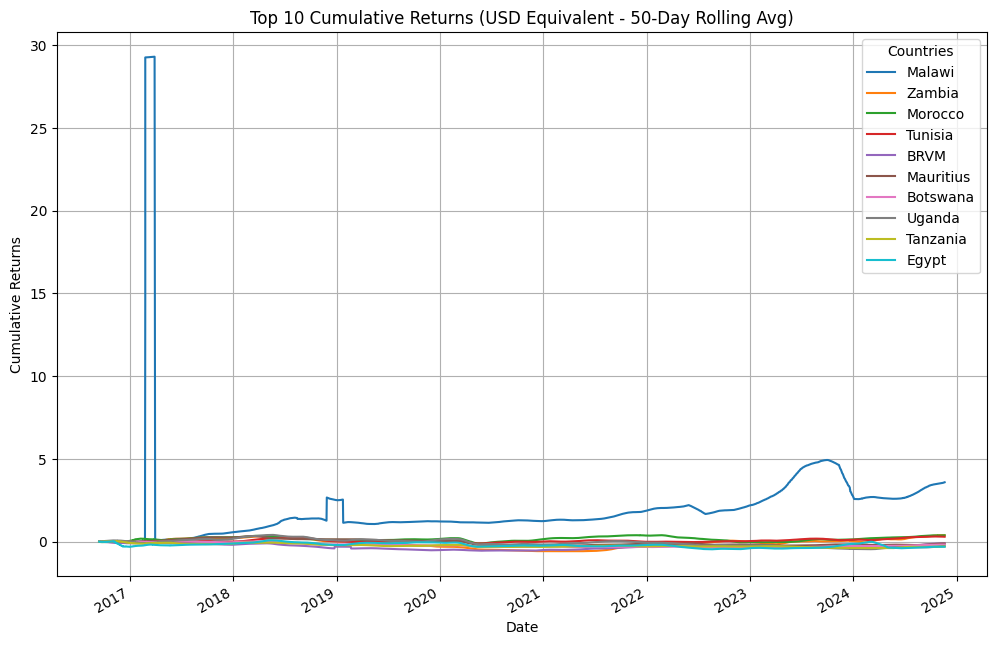

The performance analysis of cumulative returns across various African markets, in both local currency and USD terms, shows and highlights distinct patterns influenced by local economic conditions and currency fluctuations. In local currency terms, Malawi leads with a return of 10.01%, followed by Egypt (2.78%) and Zambia (2.70%), reflecting favorable domestic conditions or local currency appreciation. However, in USD terms, Malawi still outperforms with a return of 3.58%, while other countries, including Egypt, Mauritius, and Botswana, face significant declines due to currency depreciation For example, Egypt’s USD return stands at -0.31%, highlighting how local gains were offset by currency-related losses. This shows the importance of considering both local market performance and currency risk when evaluating investments.

From 13th September 2016 to 20th November 2024, the USD returns show volatility, with Malawi continuing to outperform with a 3.58% return. Egypt and Uganda, however, experience significant declines (-0.3121% and -0.2631%, respectively) due to weaker performance relative to the USD. Morocco, on the other hand, shows a cumulative return of 3.802%, indicating favorable market conditions and currency strength. In contrast, Mauritius, Tunisia, Botswana, and Nigeria display moderate returns, with Mauritius even reporting a slight loss.

The period from April 2023 to November 2024 shows consistent upward growth for Malawi, with returns ranging from 3.01% to 3.58%. This is driven by favorable local conditions or currency movements. Conversely, Kenya, Mauritius, and Nigeria display moderate fluctuations, with Kenya and Nigeria experiencing negative returns at certain points. Morocco’s performance stands out with positive returns, reinforcing regional disparities. Despite Malawi’s strong returns, the growth remains restrained, typically under 14%, indicating stable but cautious growth within broader regional market dynamics.

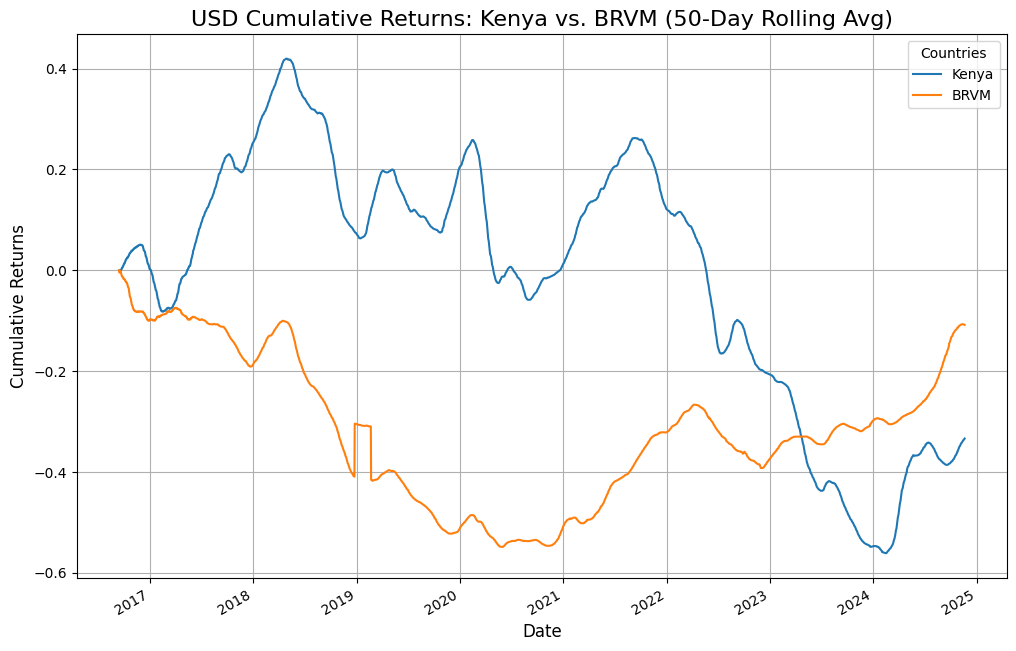

Summary statistics for USD cumulative returns emphasize the varying performance across countries. Malawi’s mean return of 2.11% outperforms other markets but shows high volatility (standard deviation of 3.89%). In contrast, Kenya and Egypt show negative mean returns of -0.01% and -0.21%, respectively, indicating overall declines. Morocco, Tunisia, and the BRVM display more stable returns, with lower standard deviations, highlighting their relative stability compared to markets like Malawi with higher risk.

The cumulative returns reveal a mix of top performers, moderate performers, and underperformers. Malawi saw a maximum local currency return of 29.3%, accompanied by sharp market movements and high risks. BRVM benefited from WAEMU’s economic integration, showing strong performance in sectors like banking and consumer goods. Egypt’s strong performance was driven by consistent reforms and economic growth. However, Uganda and Ghana showed negative returns possibly due to macroeconomic instability and currency depreciation. Kenya had a mean return of -0.013, while BRVM showed -0.303. Nigeria showed high volatility but occasional positive returns.

Performance metrics such as Sharpe ratios and drawdowns highlight regional disparities. Malawi shows the highest Sharpe ratio in both local currency (29.20) and USD terms (0.0097), indicating strong risk-adjusted returns. In contrast, Botswana and Uganda have negative Sharpe ratios in USD terms, signaling poor risk-adjusted returns. Additionally, drawdowns highlight that Tunisia, with a USD drawdown of -87.47%, faced significant losses compared to markets like Malawi, which remained relatively insulated from sharp declines.

Regional Stock Markt Performance

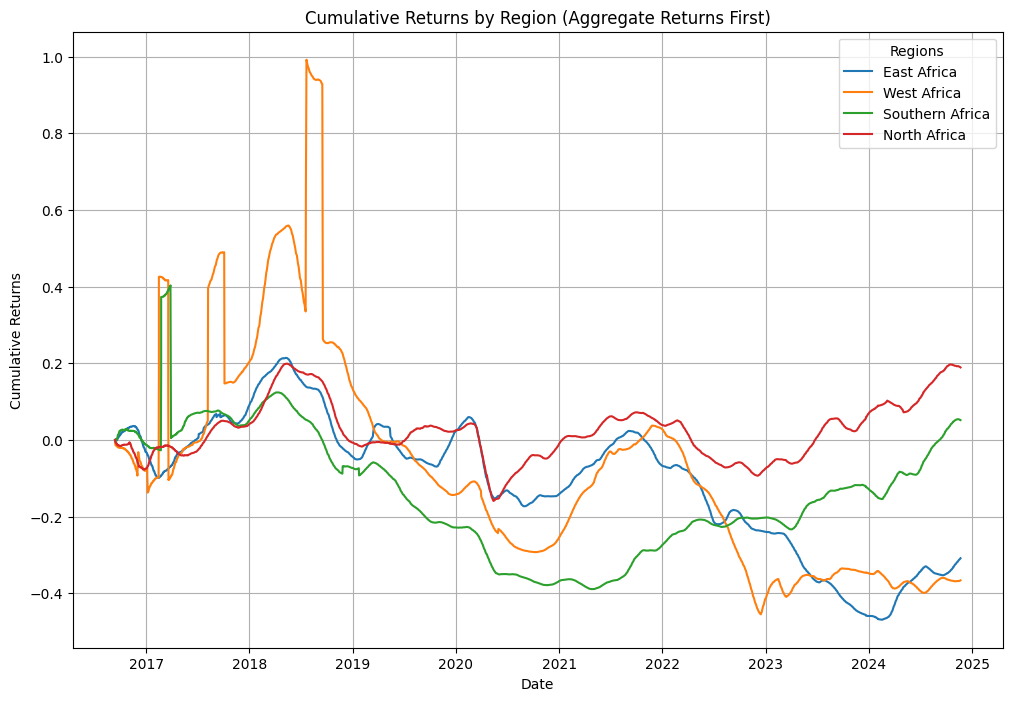

The regional performance analysis reveals significant variation across Africa, with Southern Africa emerging as a leading performer in terms of cumulative returns. Southern Africa recorded a return of 0.0518, reflecting moderate growth within the region. In contrast, East Africa and West Africa encountered challenges, with returns of -0.3084 and -0.3662, respectively, indicating notable underperformance likely influenced by economic instability, political factors, or unfavorable market conditions. North Africa demonstrated relatively stable performance, achieving a return of 0.1892, highlighting more favorable economic and market conditions compared to other regions. This regional breakdown underscores the diverse economic environments across Africa and the importance of region-specific investment approaches that align with local market dynamics and risks.

Investing 1000 USD in Stocks

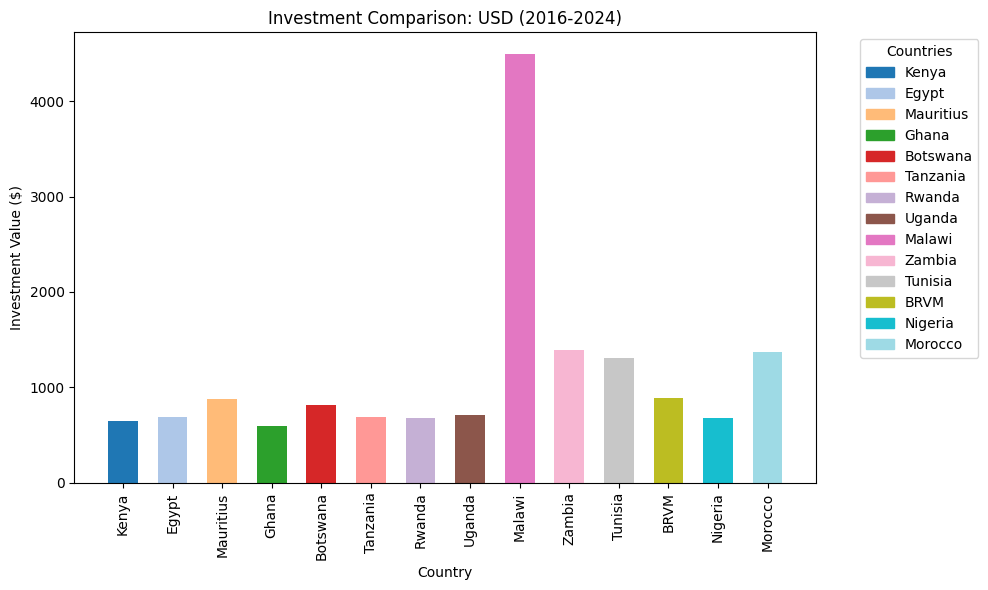

Investing $1,000 in selected African markets from January 2018 to October 2024 yields diverse outcomes influenced by currency fluctuations and market performance. Malawi and Zambia experienced significant local currency growth, with Malawi’s USD value reaching $4,499.54 and Zambia’s $1,387.53, driven by favorable local conditions despite currency volatility. Kenya saw a decline, with a USD value of $646.56 due to local currency depreciation. Ghana showed solid market performance, with a USD investment value of $594.16. Mauritius, Tunisia, Botswana, Tanzania, and Rwanda offered moderate growth, while Uganda delivered steady returns with a USD value of $707.14.

Regarding the question guiding the study Kenya Vs the BRVM… Is the BRVM doing better than the NSE, well its is an emotional question however, the BRVM (WAEMU) region saw stable returns with a USD value of $888.45, better than the Nairobi Stock Exchange (NSE)

Overall, the analysis emphasizes the significant role of currency risk in emerging markets, with varying performance shaped by local conditions, currency movements, and regional stability.

The mixed performance of African stock markets reveals both potential for growth and challenges for investors. Markets such as Egypt, Mauritius, and Malawi demonstrated strong performances, while the BRVM and NSE reflect regional strengths, yet each market presents its own unique risk profile. Currency volatility, political risks, and market structures are key factors influencing returns, emphasizing the need for a tailored and informed approach. Despite data scarcity and low market liquidity, investing in these markets could offer opportunities for diversification and growth, particularly for those seeking exposure to Africa’s economic potential without directly establishing enterprises. But does Africa offer mega returns, maybe for the private equity companies!! A well-diversified strategy can help mitigate the risks and capitalize on the rewards inherent in these emerging markets.

For a list of existing of existing stock exchanges in Africa

Written and compiled by : Simon Peter Mulima

Nice articel

Wow superb blog layout How long have you been blogging for you make blogging look easy The overall look of your site is magnificent as well as the content